Source: French to English Tester Published on: 2026-04-07

Source: The Conversation – in French– By Patrick Criqui, Research Director Emeritus at CNRS, University Grenoble Alpes (UGA)

As war and geopolitical tensions intensify in the Middle East and oil tankers now pass through the Strait of Hormuz only in dribs and drabs, the specter of a global energy shock reemerges, following a history already long marked by successive oil crises. In a world where hydrocarbon markets are more interconnected than ever, the current crisis tests the global economy and, in particular, that of importing countries. These risks reinforce the imperative to accelerate the energy transition.

After the period of “happy globalization,” the Covid-19 crisis, the invasion of Ukraine, the attack on Israel followed by its response in the Gaza territory, and today, the war against Iran, a series of crises marks the return of the world to a zone of high turbulence.

This latest event is particularly destabilizing because it affects the Arabian-Persian Gulf. If theenergy transition has begun in this region, it remains a hypersensitive area for the supply of a world still largely dependent on hydrocarbons. ForFatih Birol, Executive Director of the International Energy Agency, this is already the most significant shock to fossil fuel supply – oil and gas – in recent decades.

Beyond the threat to our economies, will this shock help accelerate their decarbonization? To appreciate its importance and transformative power, it must be placed in the long history of international energy markets, a history already rich in accidents.

Also to read:

How the Iranian revolution caused the second oil shock of 1979

Sixty years of oil crises

The occurrence of a new major international crisis in the Middle East and the threats it poses to energy supply and the global economy lead to questioning the conditions for the triggering of oil shocks. One can define aoil shocksuch as a sharp increase (a doubling, or even a tripling) and sustained rise in oil prices. Conversely, acounter-shockcorresponds to a sharp and lasting decrease.

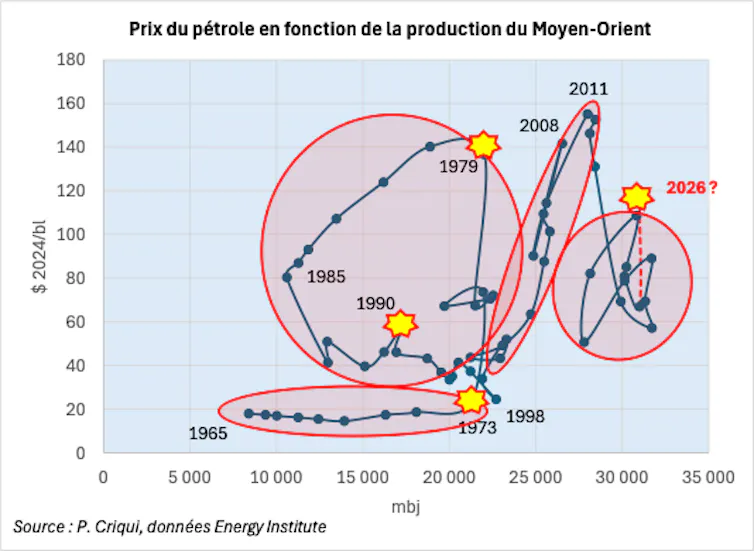

The history of oil prices over the past sixty years can be analyzed as the succession of four major periods, as shown in the figure below.

P. A. Criqui/Data: Energy Institute,Provided by the author

-

1965-1973, the rise of tensions:In the 1960s, we witnessed a very rapid increase in Middle Eastern production (a threefold increase between 1965 and 1973), with very low prices, around 20 dollars per barrel, in today’s dollars (equivalent to 17.30 euros). This caused demand to explode, which producers struggled to meet.

-

1973-1998, the time of shocks and counter-shocks:The Yom Kippur War between Israel and the Arab countries allowed them to gain control and unilaterally increase prices, which led to the oil shock of 1973-1974. A few years later, theIslamic revolution in Iranleads to a new surge in prices on emerging spot markets: this is the second shock of 1979-1980. Then a decline in Middle Eastern production (mainly Saudi Arabia) is announced, before the counter-shock of 1985-1986 and the return to a moderate price level, despite the invasion of Kuwait by Iraq in 1990.

-

1998-2015, a gradual return of tensions resulting in a third shock, this time of demand:In the early years of the 21st century, tensions re-emerged, fueled by strong global growth and the surge in raw material prices before the 2008 Beijing Summer Olympics.subprime mortgage crisis in 2008marks a halt. The price plunges, but quickly recovers to high levels, comparable to those after the second shock (around 150 dollars, just under 130 euros, per barrel).

-

2015-2025, a new balance:in the last period, a new balance is established. Despite a high level of production, particularly in the Middle East (one and a half times that of the early 2000s), and notably due to the arrival ofshale oil and gasIn the United States, the price remains in a range of 60 to 100 dollars (from over 51 euros to 86.50 euros) per barrel.

Geopolitical events and energy shocks have thus succeeded one another in the Middle East in recent decades. They are not always synchronous, but in 2026 the conditions seem well met for a “perfect storm” on energy markets: a major geopolitical event has occurred in a context of high oil production levels. And even more so since it affects another market that has become strategic: that of liquefied natural gas (LNG).

Also to read:

Why the strikes on Iran remind us that it is urgent to abandon oil

Natural gas: from regional segmented markets to a now global risk

The history of natural gas, less spectacular than that of oil, nevertheless reveals a profound transformation of the global energy system. In fifty years, gas has shifted from a system of regional markets (North America, Europe, Asia), mainly governed by long-term contracts, to a largely globalized market, a place of constant arbitrage and today exposed to major systemic risks.

Its evolution can be read in three major sequences, each marked by a supply geography, a pricing logic, and a specific degree of vulnerability.

P. Criqui,Provided by the author

-

1970–1986, the era of segmented markets:Until the mid-1980s, there was no global gas market. Natural gas was a regional product, constrained by rigid infrastructure and long-term contracts. In the United States, prices were low because it was a continental market, supplied by pipelines and regulated by federal regulations. In Europe, prices were higher because supplies relied on a mix of pipelines coming from the USSR/Russia, Norway, and Algeria, supplemented by a limited share of imported LNG. In Japan, LNG was expensive, and Asian prices were the highest in the world. These three markets communicated little with each other: no transcontinental flows, no connection between markets, no international transmission of local tensions. While there could be a global oil shock, there was not yet a global gas shock.

-

1986–2008, a relative convergence:From 1986, the structure of the markets evolved. The counter-oil shock led to a revision of contracting methods, the gradual rise of LNG trade, the opening of the first trading hubsspot market(that is to say, markets where prices are set daily) and the loosening of exchange conditions in certain regions. American, European, and Asian prices remain different, but their trends converge. This results from the development of international LNG trade, the gradual standardization of infrastructure, and the knock-on effects of a more volatile oil market. However, the period is not homogeneous. In the United States, spot markets experience very pronounced spikes due to transport constraints and regional limits on storage or production capacities. Despite these regional episodes, gas prices reflect greater international coherence.

-

2008-2025, despite the rise of LNG, a return of divergences:The third period begins with a structural shock, that of the shale gas revolution in the United States. In just a few years, the abundance of unconventional gas causes American prices to collapse. And the United States becomes, from 2016, a major LNG exporter. At the same time, Asia experiences a moment of tension after the Fukushima disaster in 2011: Japan shuts down its nuclear reactors and triggers massive LNG demand, prices soar and remain sustainably high. Europe, for its part, remains dependent on Russian pipelines until 2021. Thesituation suddenly shiftswith the invasion of Ukraine in 2022, which leads to ahistoric peak of European prices. The continent then turns to the global LNG market, placing itself in direct competition with Asian buyers for American or Qatari suppliers.

Paradoxically, the current situation marks the birth of a true global LNG market. Not because prices are converging, but because shipments are moving to the region offering the best terms. This transferability, from one region to another, of LNG cargoes effectively creates a global market, but whose prices remain divergent for the time being.

It is precisely this mechanism that explains why, in the current crisis, the blockade of the Strait of Hormuz could trigger a new global surge in gas prices. Nearly 20% of global LNG, particularly Qatari, passes through this area. The closure of Hormuz is therefore not a local risk: it is a potential global shock.

Also to read:

From the Strait of Hormuz to Europe: understanding the rapid spread of energy insecurity

Gas, an amplifier of oil crises

The current crisis differs from previous ones by its dual nature: it simultaneously affects oil and gas. In an energy system where the two markets are interdependent, this simultaneity acts as a risk multiplier.

In the short term, an increase in gas prices immediately triggers arbitrage in electrical systems:Europeas inAsia, some power plants are reverting to coal.

This phenomenon, already observed in 2022 during the invasion of Ukraine, highlights an essential reality: in times of crisis, supply security takes precedence over climate objectives. However, in both Europe and Asia, the least affected countries are those less dependent on natural gas for their electricity production because they have renewable or nuclear decarbonized sources. Notably, it is thecase of China.

But the specificity of the 2026 crisis lies in the accumulation of vulnerabilities. Oil remains exposed to the geopolitics of the Middle East, while gas now depends on global maritime routes, Asian balances, American export policies, and Europe’s ability to outbid Asia.

In other words, a local shock in the Gulf is becoming today a “stress test” (global resilience test), revealing the fragility of a now unified market, but one that is difficult to secure.

The initial market reaction illustrates this new reality: the closure of the Strait of Hormuz has not (yet) caused a massive surge in prices, but a risk premium in Europe, a convergence of Asian prices, and a marked increase in spot volatility. Traders are betting on a short blockade: it is this anticipation, more than the reality of flows, that still stabilizes prices.

The future will depend on the duration of the blockade

And so,The extent of the impacts will depend on the duration of the blockade. Beyond immediate adjustments, the issue quickly becomes macroeconomic: if disruptions persist, markets no longer balance solely through supply, but also through demand, via sustainably high prices that act as a true global energy tax, weighing on growth, purchasing power, and industrial competitiveness. But also, and this is the positive side, this could encourage decarbonization efforts.

-

For a blockage of less than three months, the impact on prices would remain limited, global flows would be reallocated, and most Asian importers would absorb the shock by using their seasonal stocks.

-

With a six-month lockdown, the tension would become structural, with more lasting price increases in Europe and Asia, and spot markets under strong pressure.

-

In the case of a blockage of about one year, the effects would resemble the 2022–2023 crisis: Asia would enter into direct competition with Europe, prices could reach extreme levels, and some emerging countries could face rationing or massive power outages.

In an energy system that is now interconnected, the determining factor is no longer just the magnitude of the shock, but its duration. The longer the crisis lasts, the more it resembles a global oil and gas shock.

It is this combination – oil, gas, maritime routes, Asian arbitrations – that creates the possibility of a true “perfect storm.” And it is also an additional reason to accelerate the phasing out of hydrocarbons, whose geopolitical vulnerability appears more clearly than ever.

Also to read:

United States shaken by their “energy domination” offensive?

![]()

Manfred Hafner is president of the energy strategy consulting firm HEAS SA

Carine Sebi and Patrick Criqui do not work for, do not advise, do not own shares in, do not receive funds from any organization that could benefit from this article, and have declared no other affiliations than their university positions.

–ref. War in Iran: a “perfect storm” for oil and gas prices?https://theconversation.com/war-in-iran-a-perfect-storm-for-oil-and-gas-prices-279893